Imagine waking up one morning and finding your refrigerator completely bare, with not a single morsel of food in sight. A sense of panic sets in, right? This scenario, though dramatic, highlights a fundamental concept in economics: scarcity. Scarcity, the fundamental economic problem, is the gap between what we want and the resources available to satisfy those wants. It’s not just about food; it applies to everything from clean water and energy to time itself. This lesson dives deep into the economic concept of scarcity, unveiling the foundations of how we make choices in a world where resources are limited.

Image: www.coursehero.com

Scarcity is the driving force behind economic decision-making. Whether you’re a consumer choosing what to buy or a government allocating its budget, the principle of scarcity dictates that choices must be made. But scarcity isn’t just a concept confined to textbooks; it’s a lived experience. Every day, we confront choices, big and small, that are shaped by the limited resources at our disposal. Understanding scarcity opens the door to navigating these choices more effectively and making decisions aligned with our values.

Understanding Scarcity

Scarcity arises because our wants are unlimited, but our resources to fulfill those wants are finite. We all have countless desires: a comfortable home, a fulfilling career, a vacation to a tropical paradise, and the list goes on. However, the means to satisfy these desires are not endless. Think about your own life: time, money, space, and natural resources are all limited. This fundamental constraint is the essence of scarcity.

The Implications of Scarcity

Scarcity forces us to make choices. We cannot have everything we want, so we must decide what matters most to us. This is where the science of economics comes in. Economics provides a framework for understanding how we make choices in a world of scarcity.

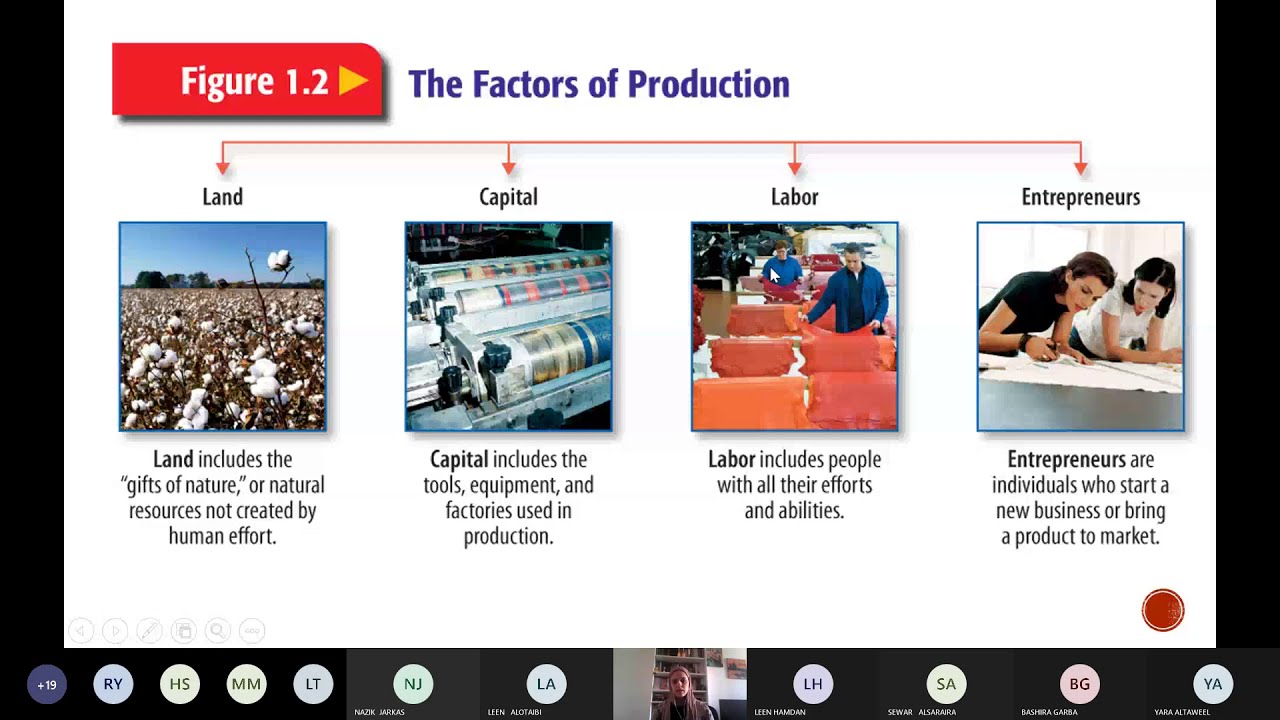

Basic Economic Concepts Linked To Scarcity

Image: www.youtube.com

1. Opportunity Cost

Every choice we make comes at a cost. The opportunity cost of a decision is the value of the next best alternative that we forgo. Consider this: if you choose to spend your weekend binge-watching your favorite show, the opportunity cost is the time you could have spent with friends, pursuing a hobby, or working on a side project. Recognizing opportunity cost helps us make more deliberate choices.

2. Trade-offs

When resources are scarce, we must make trade-offs. This involves balancing competing priorities and making choices that maximize our overall satisfaction. For instance, if you’re on a budget, you might have to choose between going out to dinner or buying new clothes. Trade-offs are an essential aspect of economic decision-making at all levels.

3. Marginal Analysis

Economics often uses marginal analysis to guide choices. Marginal analysis considers the additional benefit and cost associated with one more unit of an activity. For instance, suppose you’re deciding how many hours to work each week. Marginal analysis will help you evaluate the extra income you might earn by working an additional hour against the cost of foregoing leisure time.

Scarcity and the Allocation of Resources

The challenge of scarcity extends beyond individual decisions; it shapes the way societies allocate their resources. How does a society decide who gets what, and how much? Economics offers several approaches to resource allocation, each with its own set of consequences:

1. Market-Based Allocation

In market economies, resources are allocated through the forces of supply and demand. Prices act as signals, indicating the relative scarcity of goods and services. When something is scarce, its price tends to rise, signaling to producers to increase supply and encouraging consumers to conserve. Market mechanisms can be efficient in allocating resources, but they also lead to inequalities.

2. Government-Based Allocation

Governments often intervene in resource allocation, using policies such as taxes, subsidies, and regulations. Governments might intervene to address market failures, promote social welfare, or ensure fairness. For example, governments might impose taxes on goods that create negative externalities, like pollution, or provide subsidies for industries deemed essential to the economy.

3. Traditional Allocation

In some societies, resources are allocated based on traditions, customs, or social norms. This approach might be based on family ties, social status, or religious beliefs. Traditional allocation can be stable and predictable but can also stifle economic growth and innovation.

Scarcity in the Modern World

The challenge of scarcity is not simply a relic of the past. In our modern world, scarcity continues to manifest itself in various forms:

1. Climate Change

Climate change presents a significant challenge to the sustainability of the planet’s resources. Rising temperatures, extreme weather events, and dwindling water resources threaten to exacerbate scarcity.

2. Population Growth

A rapidly growing global population puts increasing pressure on resources such as food, water, and energy. As demand rises, scarcity becomes more acute, necessitating innovative solutions.

3. Technological Advancements

Technological advancements can both alleviate and exacerbate scarcity. For instance, innovation in renewable energy technologies contributes to the sustainability of resources. Conversely, new technologies can also increase demand for resources, leading to greater competition for scarce commodities.

Overcoming Scarcity: Strategies and Solutions

While scarcity is a fundamental economic challenge, it’s not an insurmountable one. Individuals, businesses, and governments can adopt various strategies to address scarcity:

1. Conservation and Efficiency

Conserving resources and using them more efficiently are crucial for mitigating scarcity. This involves reducing waste, developing energy-efficient technologies, and promoting sustainable consumption patterns.

2. Technological Innovation

Developing new technologies can create substitutes for scarce resources or enhance our ability to extract more resources from existing supplies. For example, innovations in renewable energy technologies can help to reduce our reliance on fossil fuels.

3. Economic Growth

Economic growth can lead to greater resource availability and enable societies to address scarcity more effectively. Investment in education, infrastructure, and research and development can foster economic growth and create new opportunities.

4. International Cooperation

Addressing global scarcity requires cooperation between countries. International agreements can help to coordinate resource management, reduce trade barriers, and share knowledge and technologies.

Lesson 1 Scarcity And The Science Of Economics

Conclusion

Scarcity, the fundamental economic problem, is an intrinsic part of our world. It compels us to make choices, to weigh alternatives, and to allocate resources wisely. While scarcity may appear daunting, understanding its dynamics empowers us to make informed choices as individuals and to advocate for policies that promote sustainability and fairness. By embracing the principles of conservation, innovation, and cooperation, we can work towards a future where the challenge of scarcity is met with solutions that benefit all.

:max_bytes(150000):strip_icc()/OrangeGloEverydayHardwoodFloorCleaner22oz-5a95a4dd04d1cf0037cbd59c.jpeg?w=740&resize=740,414&ssl=1 "What to Use for Laminate Floor Cleaner – A Comprehensive Guide")